- 1Why Generic Bookkeeping Fails a WooCommerce Store

- 2The Five Structures of Clean WooCommerce Bookkeeping

- 31. A chart of accounts built for e-commerce

- 42. One clearing account per gateway

- 53. A fee expense line per gateway

- 64. Sales tax to a liability account

- 75. Refunds as contra-revenue

- 8The Monthly Close Checklist for a WooCommerce Store

- 9Where Automation Fits (Honestly)

- 10Month-End, After

Your books aren't messy because you're undisciplined. They're messy because they were set up for a business you don't run.

Your accountant's email is three lines long: "Quick question — what's the $12,318 deposit on March 14?"

Forty minutes later, you have the answer. It's two Stripe payouts covering four days of orders, minus $402 in processing fees, minus a $618 refund from the week before, plus a $75 chargeback reversal. You know this because you opened the Stripe dashboard, exported a CSV, cross-checked it against the WooCommerce order list, and did arithmetic in a notes app.

You've been here before. Your WooCommerce bookkeeping is a folder of gateway CSVs and a QuickBooks file your accountant is diplomatically quiet about. Every month-end, you promise yourself a real system. Every month-end, you patch the current one instead.

Here's what's worth knowing before the next month-end arrives: this isn't a discipline problem, and it isn't an accounting-skills problem. It's structural. Your books were set up for a generic small business — and an online store isn't one.

Why Generic Bookkeeping Fails a WooCommerce Store

The lie underneath most messy e-commerce books goes like this: "Bookkeeping is bookkeeping. My standard small-business setup is fine for an online store."

It's a reasonable belief. It's also wrong, for five specific, mechanical reasons. A consulting firm or a coffee shop never hits these. A WooCommerce store hits all five every single day.

1. Money earned is not money deposited. A consultant invoices $1,000 and receives $1,000. Your store sells $1,000 on Tuesday, and Stripe deposits $953.90 on Thursday — bundled with Wednesday's orders. No bank deposit ever equals any sales number. If your books treat deposits as revenue, they're wrong on day one.

2. Fees are subtracted before you ever see the money. Each gateway takes its cut at the source, and each takes a different cut — Stripe, PayPal, and Square all price differently. Record deposits as income and those fees vanish: revenue is understated, and a real operating expense never appears anywhere in your books.

3. The sales tax you collect isn't yours. You're holding it on behalf of a state. Booked as income, it inflates your revenue — and then the remittance arrives as a "surprise" expense that was never an expense at all. It was a liability the whole time.

4. Refunds aren't expenses. A refund is revenue reversing, not a cost you incurred. Netting refunds silently into deposits — or worse, booking them as an expense — distorts both your gross sales and your margins, in different directions.

5. Inventory costs don't belong in the month you bought them. Expense a $20,000 stock purchase in March and your P&L shows a disastrous March and a fictional April. Cost of goods sold belongs in the month the goods actually sell, or your margin numbers mean nothing.

Each of these is invisible in a generic chart of accounts. That's why patching never works: you're not making entry errors, you're missing account structures. The fix isn't more careful data entry. It's five structures.

The Five Structures of Clean WooCommerce Bookkeeping

Get these five things set up in QuickBooks Online once, and the daily work becomes routine. Skip them, and every month-end is archaeology.

1. A chart of accounts built for e-commerce

This is the foundation the other four structures hang off. At minimum, your income section separates product sales, shipping income, and a refunds contra-account. Your expenses include one fee line per payment gateway. Your liabilities include sales tax payable. Your assets include a clearing account per gateway and an inventory account.

You don't need to design this from scratch — we've published a full chart of accounts template for e-commerce you can copy into QuickBooks in an afternoon. Do this first. Everything below assumes it exists.

2. One clearing account per gateway

This is the structure that answers "what's this deposit?" permanently.

A clearing account is a holding pen between "sale happened" and "money arrived." When you record Tuesday's $1,000 in Stripe orders, the money goes into Stripe Clearing — not your bank account, because it isn't in your bank account yet. When Stripe's payout lands Thursday, you move $953.90 from clearing to the bank and $46.10 to Stripe fees. The clearing account returns to zero (or to exactly the amount still in transit).

Now bank reconciliation means matching a handful of payouts, not hundreds of orders. And if a payout ever fails to clear, the clearing balance flags it — the money that should have arrived, didn't.

One clearing account per gateway, not one shared account. WooCommerce stores typically run two or three gateways, each with its own payout schedule. Mix them and you've rebuilt the puzzle you were trying to solve.

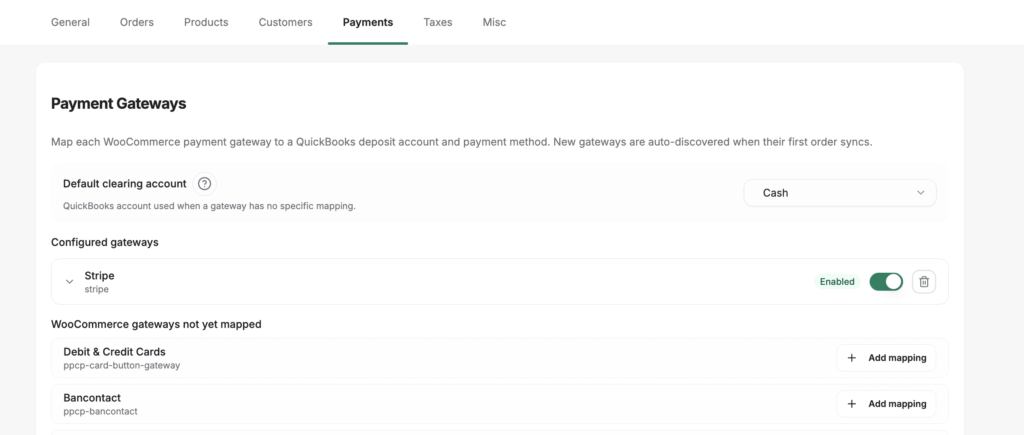

If a sync tool posts your orders, this structure is a settings page rather than a discipline. LedgerPort auto-detects every payment gateway active on your store and gives each its own configuration row — an enabled toggle, the QuickBooks clearing account where that gateway's money lands, the QBO payment method, and a per-gateway refund-sync switch — with a default clearing account as the fallback for anything unconfigured. It's exactly the structure this section just told you to build by hand; the software version only asks you to point each detected gateway at its account.

3. A fee expense line per gateway

Stripe Fees, PayPal Fees, Square Fees — separate accounts, not one "merchant fees" bucket.

Two reasons. First, accuracy: fees per gateway give you a monthly sanity check. If Stripe's effective rate is normally about 3% and this month it's 4.1%, something happened — a pricing change, a surge in international cards, a dispute fee — and you'll actually see it. Second, decisions: you can't compare what your gateways truly cost you if the costs are blended.

4. Sales tax to a liability account

Every dollar of tax collected posts to Sales Tax Payable, a liability — never to income. When you remit to the state, the payment draws down the liability. Your P&L never touches it, in either direction.

The payoff is calm: the remittance deadline stops being a cash-flow surprise, because the money was never counted as yours. The balance in Sales Tax Payable should always roughly match what your tax reports say you've collected. When it doesn't, you've caught an error early instead of at filing time.

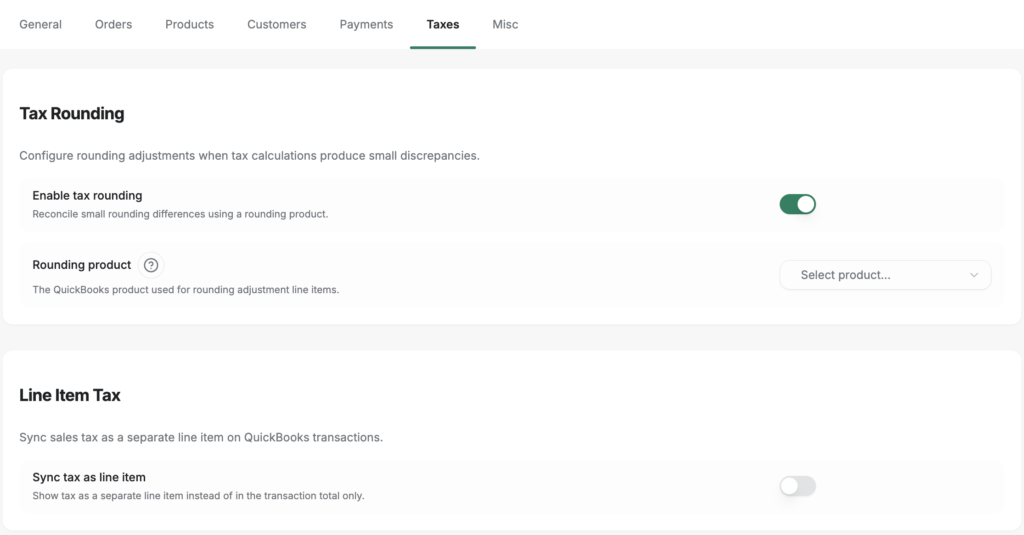

In LedgerPort, this rule is a dropdown: the Taxes tab's Line Item Tax setting posts WooCommerce tax as a dedicated line to a QBO liability account you choose — structure #4, enforced on every synced order. The same tab holds a detail almost nobody explains: tax rounding. WooCommerce and QuickBooks compute tax independently and disagree by a cent here and there; a rounding-adjustment line item absorbs those differences, so the liability account ties exactly to what you collected instead of accumulating an unexplainable few-dollars-a-month drift.

5. Refunds as contra-revenue

Create a Refunds & Allowances account in your income section that carries a negative balance. Every refund posts there — reducing net revenue while leaving gross sales intact.

This preserves two numbers you need: true gross sales (for understanding demand) and true net revenue (for understanding the business). It also surfaces your refund rate as a trackable line instead of an invisible leak. A store that refunds 2% and a store that refunds 9% are different businesses, and only one of those stores usually knows it.

These five structures are the e-commerce-specific core; for the broader habits around them, our guide to e-commerce accounting best practices covers the rest.

The Monthly Close Checklist for a WooCommerce Store

With the structures in place, month-end stops being reconstruction and becomes verification. Here's the checklist, in order:

0. Scan for Failed and On Hold records before you close. If a sync tool posts your books, this is the step that comes before everything else. In LedgerPort, every record carries one of five statuses — Synced, Pending, Failed, Skipped (intentionally excluded by your sync filters), or On Hold — so a two-minute filter for Failed and On Hold across the month catches a missed webhook while it's one order, not one quarter. The fix lives in the same screen: select the records and re-push, and the no-duplicates guarantee means already-synced records are skipped automatically while re-pushed failures update the existing QuickBooks transaction rather than posting a second one. "Hope everything synced" becomes a checkbox.

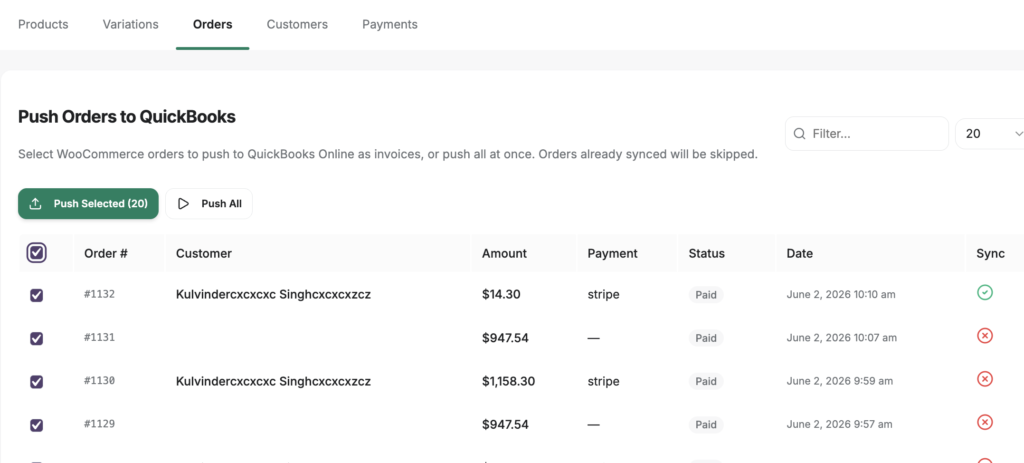

- Confirm every order is in QuickBooks. All sales for the month posted — with product revenue, shipping, tax, and gateway routing intact. If you're entering manually, this is the longest step; do it weekly, not monthly. If a sync tool is doing the posting, verify instead of re-entering: LedgerPort's audit log shows the full sync history, filterable by type, entity, status, and date, so a missed or failed order surfaces in seconds.

- Match every gateway payout to a bank deposit. Each Stripe, PayPal, and other payout should correspond to a deposit and clear the appropriate clearing account.

- Check clearing account balances. Each should equal only the money currently in transit — sales from the last day or two that haven't paid out yet. Anything more is an unmatched transaction telling you where to look.

- Review fees per gateway. Compare each gateway's fee total against its expected effective rate. A drift of more than half a percent deserves two minutes of investigation.

- Verify sales tax payable. The liability balance should match what your tax reports say you collected, less what you've remitted. Note upcoming remittance deadlines.

- Record COGS and adjust inventory. Book the cost of the units that actually sold this month; move it out of inventory and into cost of goods sold.

- Post refunds and chargebacks. Confirm they landed in contra-revenue, and glance at the refund rate while you're there.

- Run the P&L and balance sheet. Not to file anything — to read them. Margins in the expected range, no account ballooning, nothing that makes you squint. If nothing squints back, you're closed.

Done manually with clean structures, this runs one to three hours a month depending on order volume. Without the structures, the same close takes a weekend — because steps 2, 3, and 5 become forensic projects.

Where Automation Fits (Honestly)

Here's the honest version, because the dishonest version is easy to find.

Below roughly 100–200 orders a month, manual bookkeeping with the five structures is genuinely fine. The close is short, the entry volume is manageable, and a tool would be solving a problem you don't have yet.

Above that, the math shifts. Order entry scales linearly with volume, and error rates scale with fatigue. At 500–1,000 orders a month across two or three gateways, step 1 of that checklist alone can eat the hours you meant to spend running the store — and one mistyped tax amount hides in ten thousand line items.

One thing automation will not do: fix a broken chart of accounts. A sync tool pointed at generic books produces fast, automated mess. Structures first, always.

What a sync tool does do is execute the five structures continuously. LedgerPort, for example, connects WooCommerce to QuickBooks Online and posts each day's sales, fees, taxes, and refunds to the accounts they belong in — clearing accounts included — so steps 1 through 7 of the checklist are largely done before you sit down. Setup takes about 15 minutes, and there's a free plan that covers up to 30 orders a month, with paid plans from $25/month as volume grows. If you want the full walkthrough of connecting the two systems, we've written a step-by-step guide to syncing WooCommerce with QuickBooks Online.

It also lives where you already work. LedgerPort installs as a WordPress plugin, so the dashboard, mappings, sync history, and manual sync controls all sit in your wp-admin sidebar — no separate app to log into.

And the "structures first" rule gets a head start: on the Mappings page, Auto-Map compares your WooCommerce products, customers, and accounts against QuickBooks and proposes matches, marking each suggestion so you can confirm or override it before anything posts.

The trade-off worth naming: you'll still review the close. Automation moves you from doing the bookkeeping to verifying it — which is exactly where a store owner should sit.

Month-End, After

Picture the next version of that accountant email. "Quick question — what's the $14,205 deposit on the 14th?"

You don't open a CSV. You open QuickBooks, click the deposit, and see the payout journal: two days of orders, fees itemized, one refund, tax routed to the liability account. Your reply takes one line and ninety seconds, and your accountant — for the first time — responds with "great, that's everything I needed."

Month-end itself is the eight-step checklist above, a cup of coffee, and about thirty minutes. Nothing to reconstruct, because nothing was ever loose. The folder of gateway CSVs still exists somewhere, the way people keep an old phone in a drawer. You just never open it.

That $12,318 deposit took you 40 minutes to explain because five account structures were missing — not because your books needed more effort. Set up the structures this week, run the checklist at month-end, and if your order volume has already outgrown manual entry, start LedgerPort free and let it post the sales, fees, and taxes for you →

Every paid plan comes with a 14-day money-back guarantee — 100% refund, no questions asked.

Related: Chart of Accounts for E-commerce · How to Sync WooCommerce with QuickBooks Online · E-commerce Accounting Best Practices