- 1The Two Ways Recording Shopify Sales Usually Goes Wrong

- 2Why Syncing Individual Orders Breaks (and Keeps Breaking)

- 3How to Record Shopify Sales in QuickBooks Online: The Daily Summary Method

- 4Step 1 — Set up the five accounts

- 5Step 2 — Pull one day's numbers from Shopify

- 6Step 3 — Build the journal entry (worked example)

- 7Step 4 — Match the payout

- 8Step 5 — Repeat daily, verify monthly

- 9Should You Do This Manually or Automate It?

- 10What LedgerPort Does With This Structure

- 11When Recording Sales Stops Being a Task

The problem isn't your data entry. It's the recording method — and there's a reason professionals all use the same one.

You open your Profit & Loss in QuickBooks Online, and the income number is almost exactly double what you know you sold. You stare at it. You did everything the setup guide said. And QuickBooks is now telling you, with total confidence, that your store made twice as much money as it did.

If you've hit that moment, you probably got there one of two ways. Either you connected the official QuickBooks Connector (or a similar app) and followed the setup screens — and now your bank feed deposits and your synced sales receipts are both being counted as income. Or the sync worked exactly as designed and pushed every single order into QuickBooks as its own transaction, and your file now has 1,800 sales receipts for last month alone, none of which match anything in your bank feed.

Both paths start from the same reasonable belief: "I just need to find the right tutorial and enter everything carefully." That's the lie this post is here to retire. Careful entry doesn't fix either problem, because neither problem is an entry error.

The recording method decides everything. There's a specific structure — the daily summarized journal entry, flowing through a clearing account to a payout match — that professional e-commerce accountants use to record Shopify sales in QuickBooks Online. It's also the structure every serious automation tool is built on. This post walks through exactly how it works, with a worked example you can copy.

The Two Ways Recording Shopify Sales Usually Goes Wrong

Before the fix, it's worth being precise about the failure modes, because they look different but share a root cause.

Failure mode one: duplicated income. Your bank feed pulls in Shopify payout deposits — say, $1,922 lands on Tuesday. Meanwhile, your sync app has already recorded the underlying orders as sales receipts totaling roughly $2,000. If the deposit gets categorized as income (which is the bank feed's default instinct), QuickBooks now shows about $3,900 of income from $2,000 of sales. Multiply by every payout, every week, and your P&L quietly inflates until tax season, when your CPA finds it and bills you for the archaeology.

Failure mode two: the transaction flood. The sync is technically correct — every order becomes a sales receipt with line items, customer details, the works. At 50 orders a month, this is fine. At 1,500 orders a month, your QuickBooks file becomes a warehouse of individual transactions that slow down reports, make reconciliation a matching nightmare, and can push you toward QBO usage limits. You have perfect detail and zero clarity.

Different symptoms, same root cause: both approaches treat orders as the unit of accounting. They aren't. As far as your books are concerned, the unit that matters is the day — and the money that actually moves is the payout.

Why Syncing Individual Orders Breaks (and Keeps Breaking)

Here's the mechanism, because once you see it, the fix becomes obvious.

Orders are gross. Payouts are net. When a customer pays you $50, Shopify records a $50 order. But Shopify Payments deducts its processing fee before the money ever reaches you, batches your transactions together, holds them for a couple of days, and then deposits one lump sum. The deposit that hits your bank is gross sales, minus refunds, minus fees, plus or minus adjustments — often spanning parts of two different days' orders. We've written a full breakdown of this mismatch in why your Shopify payout never matches what QuickBooks shows.

So when you sync individual orders, you create income records that will never directly correspond to any bank deposit. QuickBooks sees $2,000 of sales receipts on one side and a $1,922 deposit on the other, and it has no idea they're related. You have three options at that point: categorize the deposit as more income (duplication), leave it unmatched forever (an unreconcilable bank account), or manually trace which orders belong to which payout, every time (the Sunday-night job you're trying to escape).

To be fair to the tools involved: the official QuickBooks Connector is genuinely good at what it's built for — low-volume stores that want order-level detail and are willing to manage deposits manually. The problem isn't that it's badly made. The problem is that order-level syncing is the wrong method once volume becomes real.

You tried the right solution for the problem as you understood it. The problem was just bigger than the tutorials let on.

How to Record Shopify Sales in QuickBooks Online: The Daily Summary Method

The professional method is called the daily summary (you'll also hear "daily summarized journal entry" or the "Shopify QuickBooks daily summary" approach). The idea in one sentence: record each day's Shopify activity as one journal entry that parks the net amount in a clearing account, then match the actual payout against that clearing account when it hits the bank.

One day of sales, one entry. One payout, one match. Nothing counted twice, nothing floods the file.

Here's how to build it.

Step 1 — Set up the five accounts

Your chart of accounts needs five specific accounts for this to work. Create them in QuickBooks under Settings → Chart of Accounts → New:

| Account | Type | What it holds |

|---|---|---|

| Shopify Sales | Income | Gross product sales, before anything is deducted |

| Refunds & Returns | Income (contra) | Refunds, recorded as a negative against sales |

| Shopify Clearing | Bank (or Other Current Asset) | Money Shopify has collected but not yet paid out |

| Shopify Fees | Expense | Payment processing and transaction fees |

| Sales Tax Payable | Other Current Liability | Tax you collected and owe to the state — not your money |

The clearing account is the one most people are missing, and it's the hinge of the whole method. It represents the gap between "a customer paid" and "the money reached your bank." If you want the full account structure for an e-commerce business — COGS, shipping income, gateway-specific clearing accounts — our chart of accounts template for e-commerce covers it.

Step 2 — Pull one day's numbers from Shopify

In Shopify admin, go to Analytics → Reports → Finances summary, set the date range to a single day, and pull five numbers: gross sales, refunds, sales tax collected, and (from Finances → Payouts, or the transactions export) the fees Shopify Payments charged on that day's transactions.

[IMAGE: Shopify Finances summary report with a single-day date range, with gross sales, refunds, and taxes highlighted]

Step 3 — Build the journal entry (worked example)

Let's use a fictional day with round numbers. On June 3, your store did:

- Gross sales: $2,000

- Refunds issued: $150

- Sales tax collected: $130

- Shopify Payments fees: $58

In QuickBooks: + New → Journal Entry, dated June 3. The Shopify sales journal entry in QuickBooks looks like this:

| Account | Debit | Credit |

|---|---|---|

| Shopify Clearing | $1,922 | |

| Shopify Fees | $58 | |

| Refunds & Returns | $150 | |

| Shopify Sales | $2,000 | |

| Sales Tax Payable | $130 | |

| Totals | $2,130 | $2,130 |

[IMAGE: The completed journal entry in QuickBooks Online, debits and credits balanced at $2,130]

Read what this entry just did. Your P&L now shows $2,000 of sales, $150 of refunds against it, and $58 of fees as an expense — true gross revenue and true costs, not the netted-out mush a deposit gives you. The $130 of tax sits in a liability account, because it was never your money. And $1,922 — exactly what Shopify owes you for the day — is parked in the clearing account, waiting.

Step 4 — Match the payout

Two days later, a Shopify payout of $1,922 appears in your bank feed. Instead of categorizing it as income, categorize it as a transfer from Shopify Clearing (or record it against the clearing account directly).

The clearing account drops back to zero. The deposit is explained. Nothing was double-counted, and your bank account reconciles to the penny.

If the payout doesn't zero out the clearing account, that's not a flaw in the method — that's the method working. A lingering balance means a fee changed, a refund crossed a payout boundary, or an adjustment happened, and the clearing account just told you exactly how much to go find. Payout matching at scale is its own discipline; we cover it end to end in how to reconcile Shopify payouts in QuickBooks.

Step 5 — Repeat daily, verify monthly

One entry per day, one match per payout. At month-end, two checks: the clearing account balance should equal whatever Shopify hasn't paid out yet (compare against pending payouts in Shopify admin), and Sales Tax Payable should match your Shopify tax reports before you file.

That's the entire method. Roughly 30 rows a month instead of thousands of transactions — and every row traceable to a report Shopify gave you.

Should You Do This Manually or Automate It?

Honest answer: it depends almost entirely on order volume, and the threshold is lower than most people expect.

Under ~100 orders a month, manual daily summaries are genuinely workable. You might even batch them weekly. Expect 15–20 minutes a day, or an hour or so a week. If that's you, everything above is all you need — bookmark this post and go.

Between 100 and 500 orders a month, the method still works, but the edges start to fray. Refunds landing on different days than their original orders, payouts spanning two days of transactions, the occasional dispute or adjustment — each one is a small research project. The bookkeeping is no longer hard, but it's relentless, and one skipped week creates a backlog that's painful to unwind.

Above 500 orders a month, manual daily summaries become a part-time job with a compliance deadline. This is the volume where nearly everyone either hands it to a bookkeeper (who will charge for those hours monthly, forever) or automates the entry creation. Neither choice is wrong — but "I'll just be disciplined about it" stops being a real plan around here.

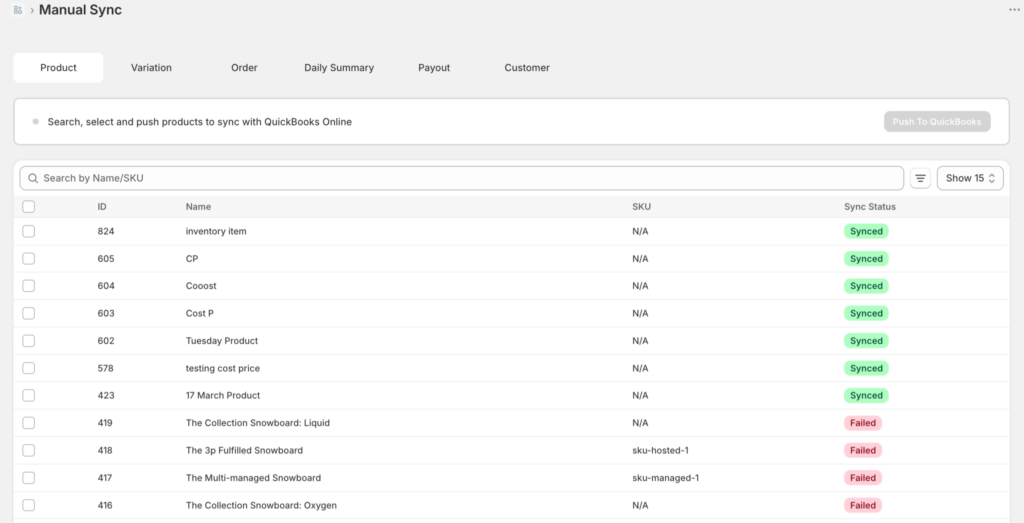

One more thing, because the binary above is slightly false: between "type journal entries by hand" and "full auto-sync" there's a middle rung — manual-but-assisted. LedgerPort's Manual Sync page lists every order that hasn't synced yet, with date-range, status, and search filters. Tick the orders you want (or Select All), click Sync Selected, and each one posts to QuickBooks as a correctly structured transaction, with a per-order Synced or Error result so nothing fails quietly. Zero data entry — but you pull the trigger.

That's exactly how the free tier works — all syncing is manual, with no restrictions on it — which makes it a zero-cost way to watch the method run against your real orders before you trust it on autopilot. Auto-sync, which runs hourly on paid tiers, is the upgrade you make after you've seen your own June 3 land in the right accounts.

Note what automation changes and what it doesn't. The method stays identical — daily summary, clearing account, payout match. Automation just builds the entries for you, every day, without being asked.

What LedgerPort Does With This Structure

LedgerPort is an example of that automation, and it's worth being specific about what it actually does, because it maps one-to-one onto the steps you just read.

It connects your Shopify store (WooCommerce too) to QuickBooks Online and builds the daily summarized journal entries automatically — gross sales, refunds, and sales tax, each routed to the right account. It separates Shopify's fees into their own expense line instead of letting them vanish inside a net deposit. And it handles the payout matching: when a payout lands, it's tied back to the clearing account so your bank feed reconciles instead of duplicating.

Daily summary isn't a workaround bolted onto a per-order tool, either. It's one of five order sync methods LedgerPort supports — Sales Receipt, Invoice, Estimate, Daily Summary, and Tag-Based — picked once in the Orders tab of the sync configuration and applied to every sync after that.

In other words: the June 3 example above, done for every day, without you opening the Finances report.

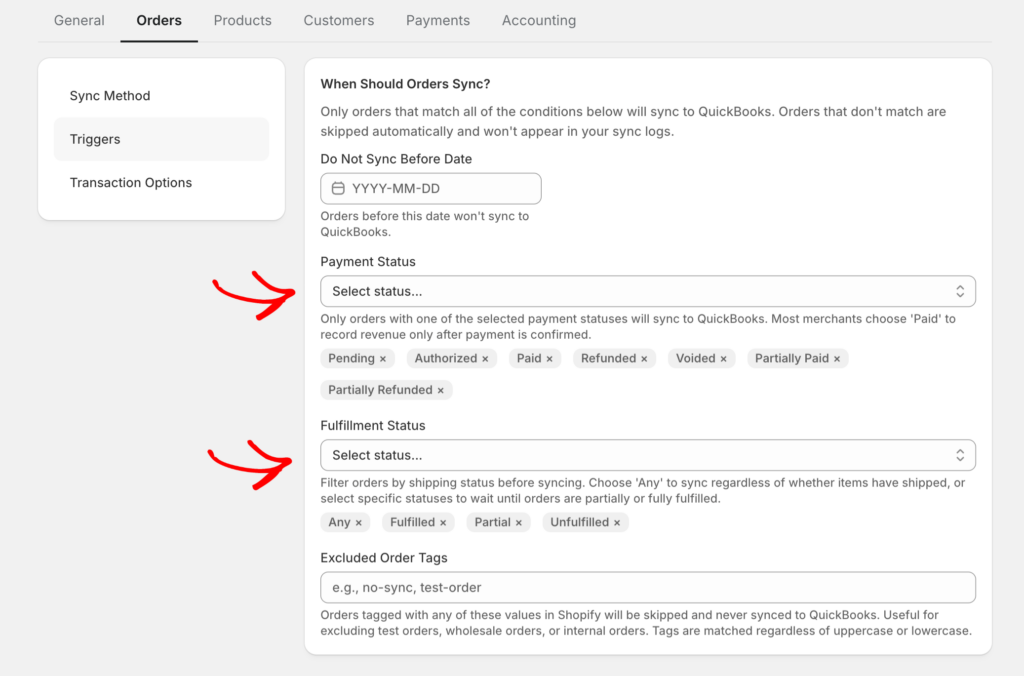

There's a subtler piece of the manual method that automation has to get right: when a sale counts. Step 2 told you to pull paid orders only — a revenue-recognition decision hiding inside a report filter. LedgerPort encodes that same discipline as sync triggers, set at Sync Config » Orders: an order posts to QuickBooks only when it meets both a payment-status condition and a fulfillment-status condition. The recommended setup for most stores is Paid plus (Unfulfilled and Fulfilled) — revenue lands in QuickBooks the moment money actually moves, regardless of shipping state. Pending and authorized-but-never-captured orders don't post, and voided orders are excluded by default, so cancellations never show up as revenue.

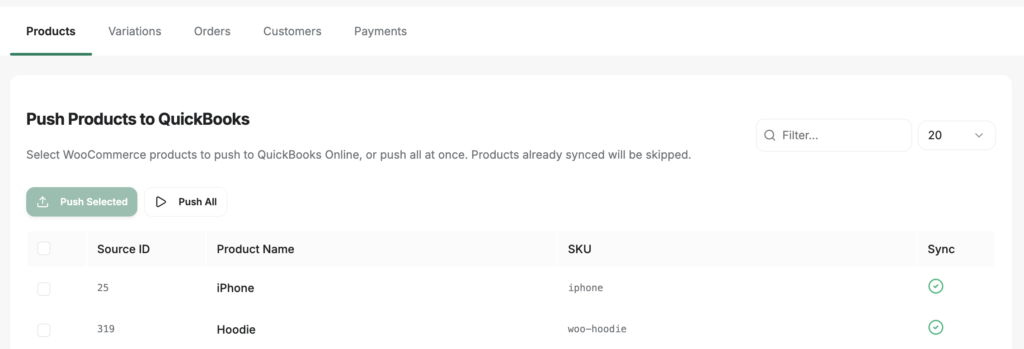

One prerequisite sits between "five accounts" and "hands-off," and it's worth naming: product mapping. Each Shopify product points at a QuickBooks item, which is what routes revenue into the right income account — and it applies to all sync methods, including Daily Summaries, not just per-order syncing. It's a one-time pass, not a project: Auto-Map matches your catalog to QBO items by SKU or product name in one click, and anything it can't match stays visibly marked Unmapped for manual cleanup rather than silently posting somewhere wrong. Together, that's the whole configuration story: the trigger decides when a sale counts, the mapping decides where it posts — and both are set once.

And the months you've already recorded the wrong way? You don't re-enter them. LedgerPort's Manual Sync page pushes historical data to QuickBooks on demand — select the records you're restating (or push them all), and a progress modal shows each one landing. Every row carries a sync status, and anything already marked synced is skipped automatically, so re-pushing after you fix a mapping won't create duplicates.

Practical details, honestly stated. Setup takes about 15 minutes — connect the store, connect QuickBooks, confirm the account mapping. There's a free plan (up to 30 orders a month, one store, manual sync on demand), which is enough to watch the method run on your real data. The Growth plan starts at $25/month for up to 1,000 orders with daily automated sync; payout journals and full fee handling come in on the Scale plan from $67/month, which covers up to 5,000 orders and three stores with real-time sync. Details are on the pricing page, and every paid plan carries a 14-day money-back guarantee — 100% refund, no questions asked.

One honest trade-off: if you want order-level detail inside QuickBooks — every customer name, every line item — a summary-based tool is deliberately not that. Summary tools exist because, for books at volume, the detail belongs in Shopify and the accounting belongs in QuickBooks.

When Recording Sales Stops Being a Task

Here's the version of this story that ends well.

It's the third of the month. Your P&L shows exactly what you sold in June — gross sales at the top, refunds and fees visible as their own lines, tax sitting in a liability account where it belongs. Every payout in your bank feed is matched. The clearing account reads zero. Your CPA sends a one-line email: "Books look clean. Nothing needed from you."

And the strangest part is what you didn't do. You didn't enter anything carefully. You didn't find a better tutorial. You stopped recording sales the way you stop noticing a door that no longer squeaks — the structure was right, so the task quietly ceased to exist.

That $2,130 journal entry from June 3 is the whole trick. You can build it by hand every morning, or you can have it built for you while you sleep. Start free with LedgerPort — it creates that exact entry from your real store data, and the first one takes about 15 minutes to see →